You have until April 15 to make last year’s IRA contribution.

But just because Uncle Sam says you can make an IRA contribution, doesn’t mean you should.

Let’s take a quick review of IRA’s:

Traditional IRA

How it works:

- You deposit money in it today.

- Your money grows for the next 10, 20, 30 years tax-free.

- You withdraw the money in retirement to buy groceries, vacation, etc.

- You pay taxes on the money you withdraw (you pay at your tax-bracket rates, NOT the lower, long-term capital gains rates.)

Roth IRA

How it works:

- You still deposit money in it today.

- Your money grows for the next 10, 20, 30 years tax-free.

- You withdraw the money in retirement to buy groceries, vacation, etc.

- You do NOT pay taxes on the money you withdraw.

I know you’re asking yourself “Why would I ever put money in a Traditional IRA? If I wouldn’t pay any taxes when I withdraw, shouldn’t I only put money into a Roth IRA?”

Spooky how I knew that, huh?

That’s a very smart question. There’s a good reason you might still want to put money in a Traditional IRA. And it depends on how much income you make today.

You need a little more info to answer that question …

There are two types of contributions you can make to a Traditional IRA:

Before-Tax Contribution (aka a “deductible contribution”)

If you make a deductible contribution, then you can deduct the contribution from your income.

Which means you’ll get a bigger tax refund… YAY! But then you’ll pay income taxes on all of it when you take it out in retirement – NOT the lower capital gains tax rates. Boo!

After-Tax Contribution (aka a “non-deductible contribution”)

If you make a non-deductible contribution, you can’t deduct the contribution from your income.

Which means you won’t get a bigger refund… BOO! But you also won’t pay income taxes on that money when you take it out. You’ll only pay taxes on the growth and interest….YAY!….but at the higher tax-bracket rates, not lower capital gains rates….BOO!

(Roth IRA contributions works this way too. You put in after-tax money. The difference is you won’t pay taxes on the growth and interest….YAY!)

So before April 15, you have 3 different IRA contributions you can make for last year:

- Roth IRA contribution

- Deductible traditional IRA contribution

- Non-deductible traditional IRA contribution

Out of the three options, which should you choose?

Uncle Sam decides for you.

How much money you make determines which contributions are allowed.

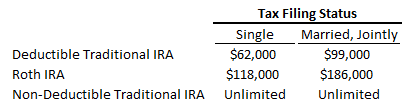

These are the limits for 2017. (For the nerds – these are all based on your Modified Adjusted Gross Income):

The rule of thumb for deductible and Roth contributions is “if you can, you should”.

If you file taxes “married, filing jointly,” and make under $99,000, you should probably make a deductible contribution to your Traditional IRA.

If you’re “married, filing jointly” and make more than $99,000, but less than $186,000, then you should probably contribute to your Roth IRA.

Like all good rules of thumb, these are just guidelines. You need to talk to your financial planner to determine if the rule of thumb applies to you. (Don’t have one? Call us!)

Current retirement savings, future retirement savings, and future income are just a few of the things that factor in.

Now comes the tricky part – if you make over $186,000 ($118,00 single) and can’t do a deductible or Roth contributions, should you make a non-deductible IRA contribution?

It’s the great white whale of personal finance – the non-deductible Traditional IRA contribution. You CAN. But SHOULD you?!?!? Bum bum buuum.

To unravel the mystery, let’s jump in our time machine. Fast forward to your 141st half-birthday.

You’re exhausted from blowing out 70.5 candles when you hear a knock at the door. It’s Uncle Sam! He wishes you a Happy Half-Birthday and reminds you that you have to take money out of your Traditional IRA today.

“But why Uncle Sam? I don’t need the money,” you ask.

“Because when you take money out of your Traditional IRA, you pay me taxes. And I needs mah taxes!” Uncle Sam replies.

It’s called a Required Minimum Distribution (RMD for short). It applies to Traditional IRA’s and BOTH Traditional and Roth 401k’s… but not Roth IRA’s. (Got that? Don’t forget we pay Congress to come up with this stuff.)

Your RMD is calculated by dividing the money you have in your IRA by an age-factor. At 70.5, the age factor is 27.4.

So if you have $100,000 in your IRA at 70.5 years old, you have to withdraw $3,650 (100,000 / 27.4 = 3,650).

Still with me?

That $3,650 IRA withdrawal counts as income on your tax return. So you’ll pay taxes on it as if you earned it from a paycheck.

Now if you have $100,000 in your IRA, adding $3,650 to your income won’t have a huge impact on your taxes.

But what if you have $100,000,0000? (Lucky you!) Then your RMD is $3,650,000. Adding $3,650,000 to your income will push you into the 37% tax bracket. That’s $1,350,500 in taxes you’re paying Uncle Sam. Oof.

Buuutttt what if your $100,000,000 was in a regular brokerage account, not an IRA? Well, none of that would have happened because RMD’s don’t apply to regular brokerage accounts.

Ah ha!

THE BIG REVEAL:

Whether or not you should make a non-deductible IRA contribution TODAY depends on how much you’ll have in your IRA when you turn 70.5.

(Warning: That’s a rather complex calculation best left to a professional. Talk to your financial planner.)

If your forecasted RMD will force you to pay a ton of taxes, then you SHOULD NOT make a non-deductible IRA contribution today. Instead, save that money in a regular brokerage account.

It won’t stop your weird Uncle Sam from coming to your 70.5 birthday party, but his visit will be a little less painful and a little less weird…. well, less painful anyways.